In today’s digital landscape, marketing compliance is a crucial consideration for banks and financial institutions. As marketing strategies evolve, so do the complexities surrounding compliance risks. Our team sat down to discuss the significant findings from recent benchmark analysis on marketing compliance risks specifically related to major U.S. banks.

Gain insights on the predictable patterns of these risks and strategies for effective oversight from this recap of our webinar, Banking Marketing Compliance: This Risk You’re Not Monitoring, hosted by Ashley Cianci, GTM Strategy & Operations; Katie Daley Infante, Director of Enterprise Sales & Partnerships; and Brilene Feyler, VP of Sales at PerformLine.

The Reality of Marketing Compliance Risks

Marketing compliance risks are often perceived as isolated incidents that occur sporadically. However, our research indicates that these risks are not random but rather concentrated in predictable areas. Key issues often arise from specific channels and types of marketing practices. Understanding where these risks frequently occur can help organizations better prepare and mitigate potential problems.

Common Categories of Compliance Risks

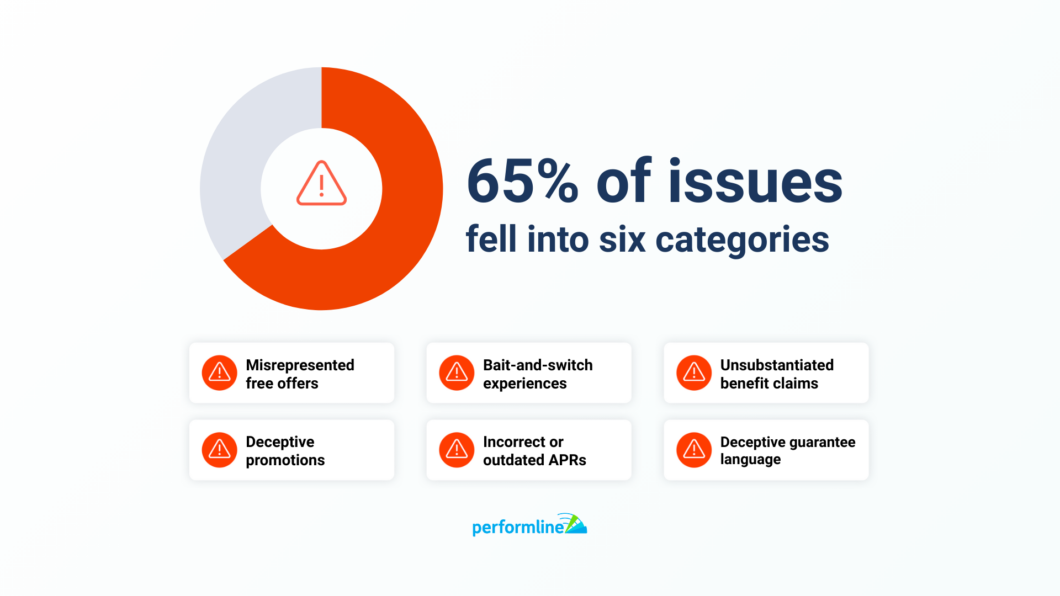

Our data revealed that 65% of marketing compliance issues fall into six main categories:

1. Misrepresented Free Offers

2. Bait and Switch Expenses

3. Unsubstantiated Benefit Claims

4. Deceptive Promotions

5. Incorrect or Outdated APRs

6. Deceptive Guarantee Language

These categories highlight the areas where banks must focus their compliance efforts, especially as marketing materials are repurposed and shared across various platforms, sometimes without adequate oversight.

Patterns of Risk in the Digital Ecosystem

A significant observation from our research is the concentration of compliance issues in affiliate and comparison sites, rather than on banks’ owned and operated channels. This insight emphasizes the importance of monitoring third-party partnerships, as these affiliates can disseminate inaccurate information quickly, leading to widespread compliance violations.

The Role of Affiliates in Compliance Risks

When banks engage with affiliates to drive consumer traffic, they may inadvertently increase their marketing compliance risks. Affiliates often have their sub-affiliates, creating a chain of responsibility that complicates oversight. According to Katie Daley Infante, PerformLine’s Director of Enterprise Sales & Partnerships, “As soon as you sign a partnership agreement, the risk of compliance issues escalates exponentially.”

When Volume Quietly Becomes Material Risk

In one recent analysis, only 8% of pages reviewed contained potential issues. That sounds small—until you zoom out to the hundreds of thousands of URLs many enterprises have in the wild. At that scale, 8% is no longer a rounding error; it’s meaningful exposure.

The tipping point is when issues stop being isolated and start showing up systematically, especially in places with very little oversight. One incorrect disclosure on a single page can be fixed by a person. The same incorrect disclosure pattern replicated across hundreds or thousands of pages is something a person—or even a team of people—simply cannot keep up with.

That’s the moment volume becomes material risk. And it’s also the moment organizations have to think differently about how they manage marketing compliance.

Why Manual Review Alone Can’t Keep Up

Many programs are built on the assumption that human reviewers can handle the risk: assign a person to look at each page, fix what’s wrong, and move on. That model works when content volume is limited and mostly lives on owned channels.

But marketing ecosystems don’t look like that anymore:

- Organizations work with affiliates, influencers, publishers, and aggregators.

- More content is being created by more people, more often.

- AI tools and generative studios can spin up hundreds of variants of an asset almost instantly.

As a result, review volume climbs from 100 assets, to 200, to 500, and then to 1,000 and beyond. You cannot keep hiring “more bodies” in compliance to match that curve, especially when budgets are being cut and headcount is under pressure.

This isn’t just a resourcing problem; it’s a structural one. Manual, person‑by‑person review wasn’t designed for exponential scale.

Importance of Pre-Publication Review

To effectively manage marketing compliance risks, a robust pre-publication review process is essential. Compliance teams often face pressure to expedite marketing campaigns, which can lead to oversights in compliance checks. Katie emphasizes the need for a centralized system to manage disclosures and promotional language to ensure that all marketing materials are compliant before launch.

Challenges in Disclosure Management

Disclosure management is inherently challenging due to the volume of assets that require approval and the constant updates needed for accuracy. As Katie points out, maintaining compliance at scale across various marketing channels is a considerable challenge that requires automation and effective control measures.

Real-Life Examples of Compliance Issues

Understanding the real-world implications of compliance violations is crucial.

EXAMPLE 1: A bank that faced significant consumer complaints due to a miscommunication about a promotional offer. A simple typo by an intern was picked up by an affiliate and led to widespread misinformation before it was caught 30-45 days later, illustrating how minor mistakes can have dramatic consequences in the digital age.

EXAMPLE 2: A larger bank who signed on a new nonbank partner, who doesn’t necessarily know all of the relevant banking roles. This partner went live with a promotion stating the rate as 4% instead of 4.01%, [example rates] which might be a minor issue to someone on the nonbank marketing team but could lead to serious enforcement if left uncorrected.

How to Communicate Marketing Compliance Exposure with Leadership

An important theme from the conversation: the goal of compliance is not to stop growth. The goal is to help the business grow safely.

What often changes the conversation internally is how the risk is framed. Executives don’t tend to fixate on a single violation on a single web page. Instead, they care about:

- Consumer impact

- Regulatory exposure

- Overall brand risk

- Strategic growth

They want to understand: Is this a repeatable risk that can get out of control? Is it a systemic issue, not just a one‑off? And what resources or solutions will allow us to reduce that risk while still pursuing our growth goals?

It’s really moving the conversation away from specific instances into more systemic exposure…this has gone from being isolated incidents to truly like a systemic issue, something that is bigger than us. And executives want to know “How do we reduce risk while still allowing the business to grow?”. They’re thinking from that strategic growth.

– Brilene Feyler, VP, Sales, PerformLine

Teams have more success with leadership when they:

- Shift from talking about isolated incidents to systemic exposure.

- Connect risk reduction to growth (“we can safely expand affiliates, influencers, and new channels if we get this under control”).

- Bring solutions along with problems—guardrails, technology, and processes that enable marketing to move faster, not slower.

Leadership responds far better to “here’s how we grow safely” than to a list of problems with no path forward.

Friction Between Marketing And Compliance Teams

As marketing programs scale, friction between marketing and compliance tends to surface in two big areas:

- Speed and scale

- Marketing wants to get new products, campaigns, and partners to market quickly.

- They often try to “take some of the compliance work off the compliance team,” asking: how can we get this asset as compliant as possible ourselves?

- The theory: if you can create something that’s closer to compliant on the first try, you avoid endless iterations and move faster.

- Lack of standardization and clarity

- Content creators didn’t go to law school and don’t have licenses.

- They don’t always understand why a disclosure that worked last week suddenly needs to change because a single phrase shifted.

- Without standardized, accessible guidance, compliance can feel mysterious and inconsistent.

That’s why a “middle layer” becomes so important. Something that standardizes feedback, applies rules consistently, and bridges the gap between what marketing is trying to do and what compliance needs to see. Done right, that middle layer doesn’t slow marketers down—it actually helps them get to market faster with fewer surprises.

Increase your speed to market with PerformLine.

The Biggest Misconception: “If We Didn’t Make It, It’s Not Our Problem”

When it comes to marketing compliance risk, one misconception stands out: “If I didn’t produce it, it’s not my problem.”

A close cousin: “We didn’t know it was out there, so we shouldn’t be accountable for it.”

In practice, this often looks like:

- Ignoring affiliate or third‑party content because it’s “their” page.

- Assuming that if the bank didn’t directly publish something, regulators won’t connect it back.

- Hoping that not looking too closely will make the risk go away.

“Playing ostrich”—putting your head in the sand and hoping the problem disappears. That posture does not play well in an exam or consent order.

-Katie Daley, Enterprise Sales & Partnerships

Regulators do not tend to say, “You didn’t know this was out there? No problem.” More often, the response is a hefty fine and an expectation that you’ll learn from your mistakes.

– Brilene Feyler, VP, Sales

The real choice for organizations is: do you want to learn after you’ve been labeled a bad actor, or do you want to know about issues early and fix them before they become enforcement actions?

Regulators expect accountability regardless—ignorance isn’t a defense.

A Shifting Regulatory Landscape (And Why It Still Matters)

Another nuance in today’s environment is that oversight doesn’t feel the same everywhere. In some areas, there’s a perception of reduced federal enforcement. At the same time, states and attorneys general have become increasingly active.

That means:

- Multi‑state institutions can face many different regulators with different expectations.

- Requirements can vary across states, products, and channels.

- The landscape is constantly changing, and teams are trying to keep up while still doing their day‑to‑day work.

This is stressful for compliance teams, especially when they know the “pendulum” can swing back toward more aggressive enforcement at any time. There’s also the risk of a look‑back period: what feels acceptable in today’s environment might be scrutinized years from now.

The banks described in the conversation are not reducing oversight just because federal pressure seems lighter in some areas. They know that staying proactive now is far less painful than scrambling to catch up later.

The New Marketing Reality: AI and LLMs

The marketing ecosystem itself is evolving quickly, driven in large part by AI and large language models (LLMs). Consumer behavior is changing too.

We’ve gone from Googling everything to asking assistants for direct answers. People are already asking AI tools questions like:

- Which credit card should I choose?

- What loan is best for me?

- Who has the best HELOC rates?

Those answers are being generated from content that’s already out there on the web. And that’s where the risk grows:

- Some AI‑recommended URLs for major brands aren’t actually owned by the brand.

- In some cases, those URLs can even point to phishing sites.

- AI is pulling from owned, third‑party, and unknown content alike.

In other words, if your “house” is messy—outdated offers, inconsistent disclosures, misleading third‑party descriptions—AI is going to learn from that mess. And many consumers are not double‑checking those results. For them, the AI answer is the research.

At the same time, marketers are using AI to generate content at unprecedented scale. More versions, more personalization, more campaigns. That only amplifies the need for guardrails and oversight that can keep up.

Whether or not an organization is intentionally advertising through AI‑driven channels, it is already being talked about, summarized, and recommended there. Ignoring that reality is just another version of the ostrich strategy.

📋

Download The Proactive Guide for AI‑Generated Marketing Assets for 7 steps to a proactive defensible marketing compliance program

Working together with content creators

Pre‑publication review is essential. It governs what gets launched and helps ensure that the first version of an asset is compliant.

Continuous marketing compliance addresses:

- How to monitor content spreads across affiliates, influencers, or publishers.

- Content changes over time as offers age or get reused, discovering unknown/not-owned brand presence across the web is crucial for brand protection

- Discover multiple channels where you don’t directly publish, but where you are absolutely being discussed.

Leading institutions are evolving their oversight models by:

- Moving “upstream,” closer to content creation, so creators get feedback in real time instead of only at the end.

- Using that upstream guidance as a first line of defense, so compliance reviewers see higher‑quality assets and spend less time on basic fixes.

- Building frameworks that allow marketing to move quickly and scale safely, while still maintaining visibility and accountability across internal teams and external partners.

A key signal of maturity is when teams recognize they can no longer just react to individual issues—they need a process that manages patterns, not just incidents.

Expanding Your Marketing Compliance Reach Beyond Pre-Publication Review

Pre-publication review remains a cornerstone of effective marketing compliance—it’s the essential first line of defense that ensures high-risk assets and new campaigns meet your standards before they launch. Leading institutions are now building on this strong foundation by extending oversight across the full content lifecycle.

Even with rigorous pre-publication controls, content naturally evolves once it’s live:

- Affiliates may adapt language or rates from your approved materials

- Influencers interpret products in their own voice

- Third-party sites aggregate or repurpose your offers

- AI tools draw from publicly available information about your brand

Forward-thinking programs enhance pre-publication review with complementary capabilities that provide comprehensive visibility:

- Ongoing monitoring of web, social, email, SMS, affiliates, publishers, and partner channels

- Consistent rule application across both owned properties and external environments

- Streamlined remediation processes with clear workflows and timelines

This lifecycle approach lets your team maintain the quality established during pre-publication review while adapting to how content actually performs in the real world. Technology plays a key role by surfacing potential issues, prioritizing by risk level, and creating a clear record of proactive oversight across your entire marketing ecosystem.

Read more about Why Banks Miss Marketing Compliance Risk After Content Goes Live

“The Struggle” As A Signal Of Maturity

One phrase from the webinar captures this perfectly:

“The struggle is the signal of maturity.”

When marketing and compliance are:

- Battling over speed versus scrutiny,

- Feeling like they’re “busting at the seams,”

- Seeing that current processes are no longer scalable,

That’s not a sign the program is failing. It’s a sign the organization has outgrown its old model and is ready for a more mature one.

At that point, the most effective organizations:

- Acknowledge that their existing approach won’t scale further.

- Align on clear, shared processes that everyone can understand and follow.

- Put consistent guardrails in place across channels and partners.

- Embrace technology and smarter workflows so they can do more with less.

Stay Ready So You Don’t Have To Get Ready

If there’s one piece of advice from the discussion on how to design marketing compliance oversight today, it’s this:

Stay ready so you don’t have to get ready.

Don’t wait for an exam finding or consent order to be the catalyst for investing in better oversight. Don’t wait until someone makes an example out of your brand. The most proactive organizations:

- See marketing compliance as a catalyst for growth, not a constraint.

- Empower creators with clear standards and tools so they can be more independent.

- Reduce internal friction by giving everyone shared, transparent guardrails.

- Treat foresight and proactivity as core parts of their strategy, not nice‑to‑haves.

The issues you’re seeing today are likely to repeat and scale as your marketing grows. The question is not whether they’ll grow—but whether you’ll be ready for them before they become material risk.

To catch this full webinar on-demand go to: Banking Marketing Compliance: This Risk You’re Not Monitoring.

See how PerformLine gives you automated oversight, clear evidence, and a workflow that supports both speed and efficiency. Request a demo to see it in action.

FAQs

The majority of marketing compliance fell into six categories that include misrepresented offers, bait and switch experiences, unsubstantiated claims, deceptive promotions, incorrect APRs, and deceptive guarantee language.

Compliance issues can arise from affiliate marketing due to the lack of visibility and control over how products are represented by third parties, leading to potential marketing compliance issues.

Banks can improve pre-publication review processes by maintaining a centralized system for disclosures and ensuring that marketing materials are thoroughly vetted for compliance before launch.