Your pre-publication review process is working exactly as designed. Legal reviewed it, compliance approved it, and it went live. From your team’s perspective, the file is closed.

The exposure window, though, is just getting started.

Approval controls what goes out the door. It doesn’t control where content lands once it leaves.

For large banks with co-branded products, affiliate relationships, and partner ecosystems, the distance between “published” and “fully accounted for” can be significant—and that gap is where marketing compliance risk quietly accumulates.

Why good internal processes still miss risk

Pre-publication review was built for a specific job: catching problems before content is distributed. It does that job well. The gap isn’t in the review itself, it’s in the assumption that distribution ends at your owned channels.

Once content is approved and published, your team moves on. New campaigns come in, new reviews get queued, and the previous content is treated as settled. But that content doesn’t stay still. Partners pick it up, affiliates republish it, comparison sites pull product details and display them independently, often without any notification to your team.

By the time that content has spread across the web, it may be outdated, decontextualized, or inconsistent with your current terms—and your compliance program has no visibility into any of it.

Where content goes once it’s published

PerformLine’s benchmark analysis of leading U.S. banks found thousands of web pages associated with each institution’s brands and products—and a significant portion of those pages weren’t owned channels. They were third-party sites, partner pages, affiliate placements, and comparison tools that sit entirely outside a bank’s direct control.

This is the norm for large banks. Your brand shows up in places you didn’t put it, alongside messaging you didn’t write, promoting products under terms you may no longer offer.

Without continuous, automated discovery, there’s no reliable way to know what’s out there until something surfaces through a complaint, an exam, or a consumer dispute.

Risk in action: an outdated APR still live on a partner site

Here’s how that plays out in practice:

A federal rate change triggers an APR update. Your team moves quickly, owned pages are updated within days, and internal systems reflect the new rate. From your team’s vantage point, the update is complete.

But a comparison site that promotes your product still shows the old rate. That page wasn’t on anyone’s update list, because no one knew it existed. A consumer finds it through a search, sees a rate that’s two percentage points lower than your current offering, and makes a decision based on it. By the time they reach the application, the rate they were shown is no longer accurate.

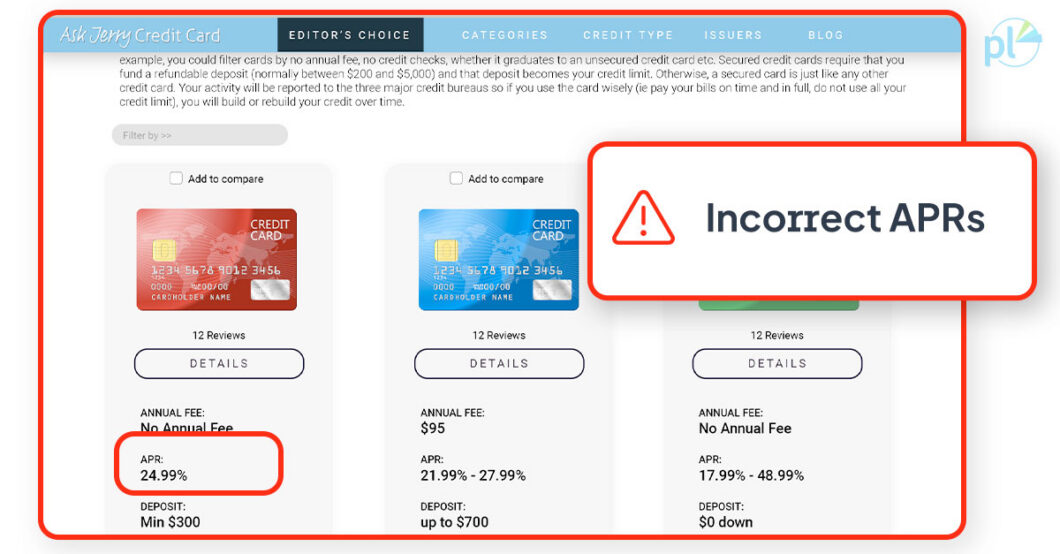

PerformLine’s benchmark surfaced exactly this type of discrepancy.

One example showed an APR of 24.99% still live on a third-party page while the current rate was 26.99%.

Rate changes can ripple across hundreds or thousands of external pages, and even short delays create real exposure—particularly when consumers are actively comparing products and relying on that information to make financial decisions.

How automated discovery and continuous monitoring changes the game

Most compliance teams are monitoring the channels they know about. The problem is that knowing about them in the first place requires discovery—and that’s where many programs have the biggest gap.

Manual discovery methods like periodic audits, sampling, and spot checks can catch issues in places your team already knows to look. They don’t scale to the volume of content associated with a large bank’s brand, and they won’t surface the partner pages, affiliate placements, or comparison sites that no one knew to look for in the first place.

You can have rigorous monitoring in place and still miss a significant portion of your actual risk footprint.

Automated discovery changes that baseline. Rather than building a monitoring program around a known list of pages, you’re continuously expanding that list—finding new placements, unknown pages, and external content tied to your brand before they become a problem.

Monitoring then evaluates that content against compliance rulebooks on an ongoing basis, flagging specific pages with specific issues rather than waiting for something to surface through a complaint or exam.

PerformLine’s benchmark found that banks using automated discovery and continuous monitoring achieve roughly 3x greater brand protection coverage across the web compared to manual search and review alone.

That coverage gap is the difference between a compliance program that knows what it’s looking at and one that’s only seeing part of the picture.

How one financial institution saved an equivalent of 3,100+ hours on APR updates

A leading global financial institution managing co-branded credit card products was facing this problem head-on.

Every time the Federal Reserve adjusted the prime rate, the compliance team had to manually locate and update web pages, often working early mornings and late nights to keep pace.

The institution had products being promoted across thousands of external pages, with no efficient way to identify which ones included APR information and which of those actually needed to be updated. The team was reviewing every page individually just to find the ones that required action.

After implementing PerformLine’s Discovery and Web Monitoring, the platform monitored more than 59,000 web pages associated with the institution’s brand and automatically flagged only the pages with outdated APR information. The team went from manually reviewing everything to focusing exclusively on the pages that required their attention.

The result: more than 3,100 hours saved compared to their previous manual process, with a scalable system in place for every future rate change or regulatory update. When the next prime rate adjustment comes, they’re ready.

How much of your content lives outside your line of sight?

The risks highlighted in PerformLine’s benchmark aren’t the result of weak compliance programs. They’re the result of incomplete visibility.

Your organization can’t monitor what it can’t find.

We’re offering banks a personalized Marketing Compliance Risk Snapshot that shows you exactly where your brand and products are showing up across the web and which compliance issues are most prevalent for your institution.