In our latest benchmark of marketing compliance risk across 25 leading U.S. banks, PerformLine uncovered thousands of web pages promoting bank brands and products across the broader digital ecosystem.

Most of the flagged risk did not appear on owned websites. It was found on third-party pages, including affiliate sites, partner placements, and comparison platforms where bank marketing had been republished or adapted.

Across this benchmark, 65% of flagged content fell into just six recurring categories, reinforcing that these issues follow consistent and repeatable patterns.

The examples below were all discovered on pages not owned by the banks included in our analysis. They reflect the types of violations that often go unnoticed until surfaced through scalable discovery and monitoring.

Below are actual marketing compliance violations flagged using PerformLine’s discovery platform.

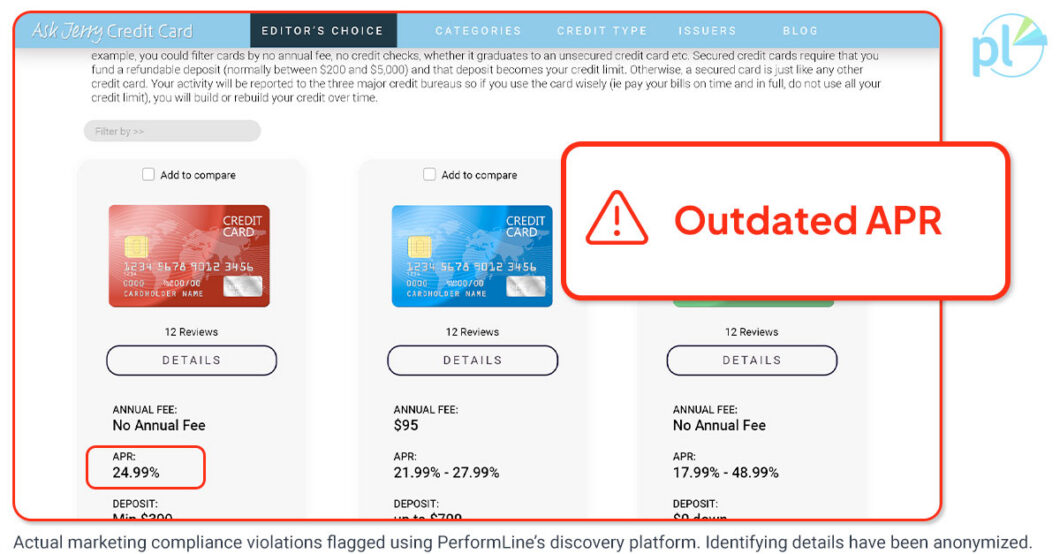

1. An outdated APR still live on a third-party page

In this example, the APR displayed is outdated and does not reflect the current rate, which could mislead consumers about the true cost of the product if relied upon during decision-making.

Consumers expect advertised rates to reflect current terms. Regulators and internal stakeholders do as well. When interest rates shift, marketing content must be updated quickly. Even brief delays can create exposure, particularly if outdated APRs remain visible on third-party pages that consumers continue to reference.

For large banks, the challenge is rarely intent, but rather scale.

A single rate change can trigger updates across hundreds or thousands of pages, many of which fall outside direct control.

If some of those placements are overlooked, inaccurate APRs can remain live long enough to generate confusion, complaints, or heightened scrutiny during reviews and examinations.

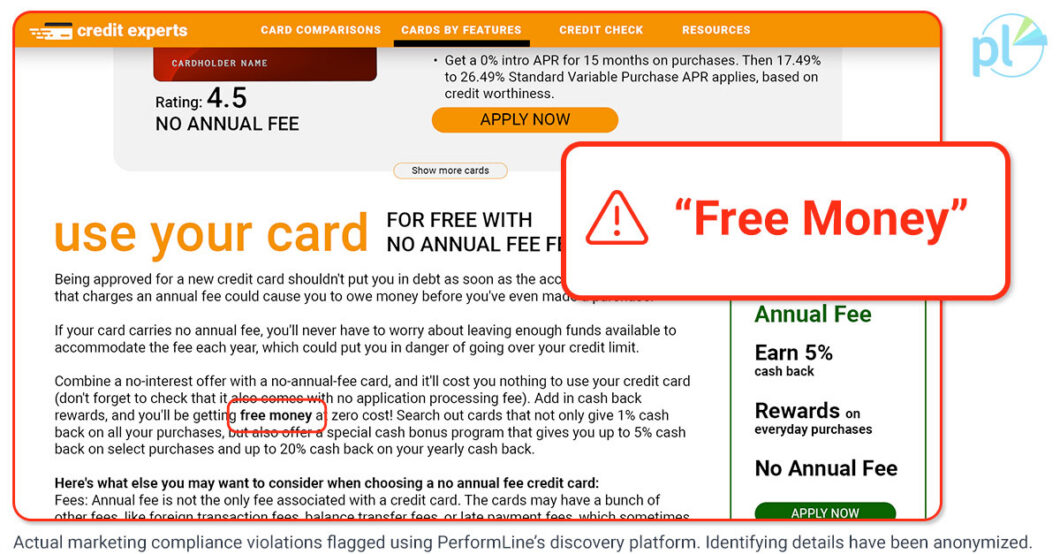

2. “Free money” that wasn’t fully explained

In this example, “free money” implies an unconditional benefit, even though rewards are typically subject to spending thresholds, caps, or other conditions.

“Free” language can shape consumer perception immediately.

If qualifying terms are unclear, buried, or presented inconsistently, consumers may interpret the offer as unconditional and costless.

When the full requirements surface later, the gap between expectation and reality often results in confusion, complaints, and closer examination of the marketing practices involved.

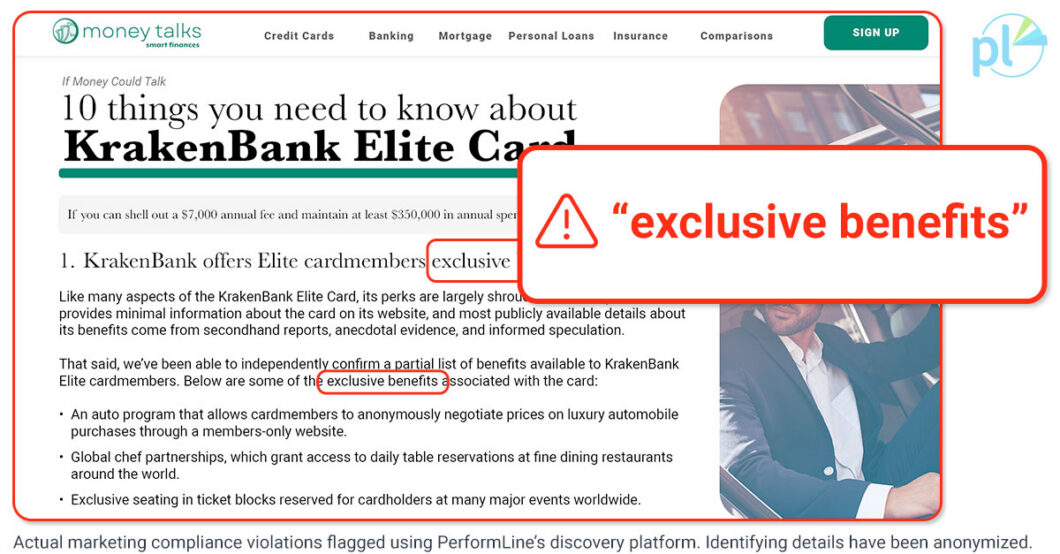

3. “Exclusive Benefits” Without Clear Support

In this example, “exclusive benefits” could imply guaranteed or broadly accessible perks, even though availability, eligibility, or access may be limited, conditional, or not clearly substantiated for all cardmembers.

Promotional language like this that overstates benefits can erode trust when it appears on pages consumers connect to a bank’s brand.

If the experience does not align with the claim, frustration follows. Complaints increase, and reputational impact grows, particularly when similar wording appears across multiple third-party sites outside the bank’s direct oversight.

These patterns also tend to attract attention during internal reviews and regulatory examinations. Repeated or exaggerated claims can point to weaknesses in marketing controls and third-party monitoring, regardless of who originally published the content.

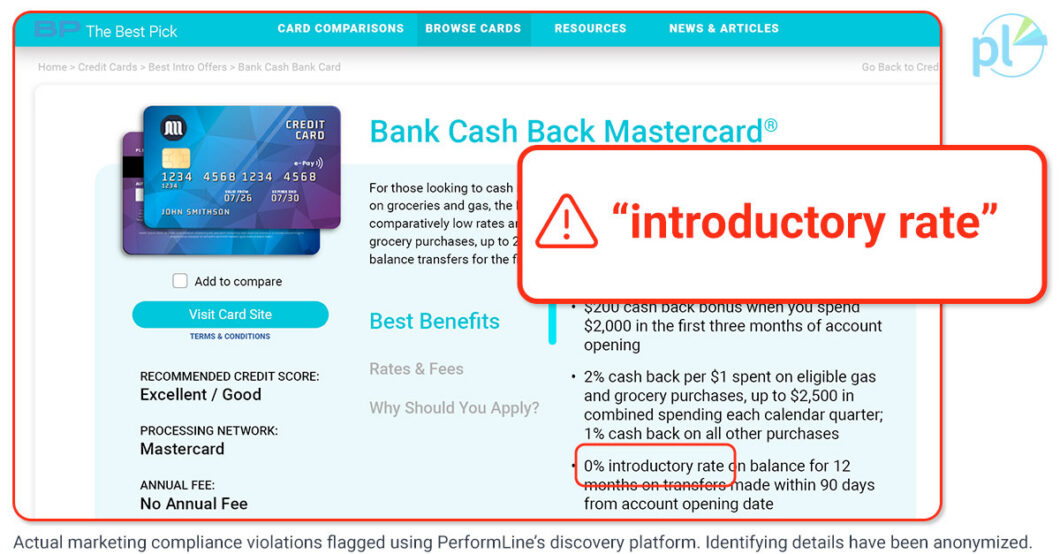

4. An Introductory Rate That Shifts After Engagement

In this example, “introductory rate” may draw consumers in with a favorable short-term offer, but the rate can later shift to significantly less favorable terms once the introductory period ends, creating a misleading expectation if those conditions are not clearly communicated upfront.

This type of issue often becomes apparent at the point of engagement, such as after a click or application start, when expectations are tested against actual terms.

If the transition between promotional and ongoing rates is not clearly conveyed, trust erodes quickly.

For large banks, these experiences carry reputational impact because consumers tend to attribute the entire journey to the brand. When terms appear to change unexpectedly, complaints increase and confidence in the digital experience declines.

What these examples have in common

None of these examples necessarily involve extreme or obviously deceptive language. They can look like standard marketing copy—which is why they matter.

Many of these issues persist because institutions lack scalable marketing compliance monitoring across third party websites, affiliate partners, and comparison platforms.

Across our benchmark, 65% of flagged content fell into six recurring issue categories, including outdated APRs, misrepresented free offers, deceptive promotions, bait and switch scenarios, unsubstantiated benefits claims, and misleading guarantee language.

Discovery is often the missing piece of mitigating these risks. Many of the pages flagged during this benchmark were previously unknown to the institutions involved.

Is this happening to your bank?

Marketing compliance risk does not stay confined to owned websites. It spreads across the broader digital ecosystem, often without clear visibility.

The examples above are only a sample of what we uncovered. The full benchmark report includes additional anonymized screenshots, deeper analysis, and data on how risk is distributed across owned and third-party placements.

If you want to explore the full findings, download the full report.

If you want to understand what this looks like for your own institution, request a personalized Marketing Compliance Risk Snapshot from PerformLine. It shows where your brand appears across the web, which issues are most prevalent, and where to focus first.